The Austrian Sustainability Reporting Act (Nachhaltigkeitsberichtsgesetz, NaBeG) which transposes the Corporate Sustainability Reporting Directive (CSRD) and parts of the EU Sustainability Omnibus Package (Omnibus I), recently entered into force. This blog post provides an overview of Austria’s NaBeG and outlines key considerations for businesses as the Austrian sustainability reporting framework evolves.

Background: The CSRD & the EU Sustainability Omnibus Package

The CSRD mandates comprehensive sustainability reporting for entities of public interest (PIEs), large EU companies and EU subsidiaries of global non-EU undertakings within its scope. These entities must include a dedicated sustainability section into their annual (group) management reports, covering a wide range of environmental, social, and governance (ESG) information. Reporting is guided by the European Sustainability Reporting Standards (ESRS), using a double materiality assessment of a company's impacts, risks, and opportunities. In response to concerns over the breadth and complexity of CSRD obligations, Omnibus I was adopted by the European Parliament in December 2025 and will enter into force on 18 March 2026, providing significant streamlining of the EU’s corporate sustainability reporting framework (for more details regarding Omnibus I, see our previous blog post).

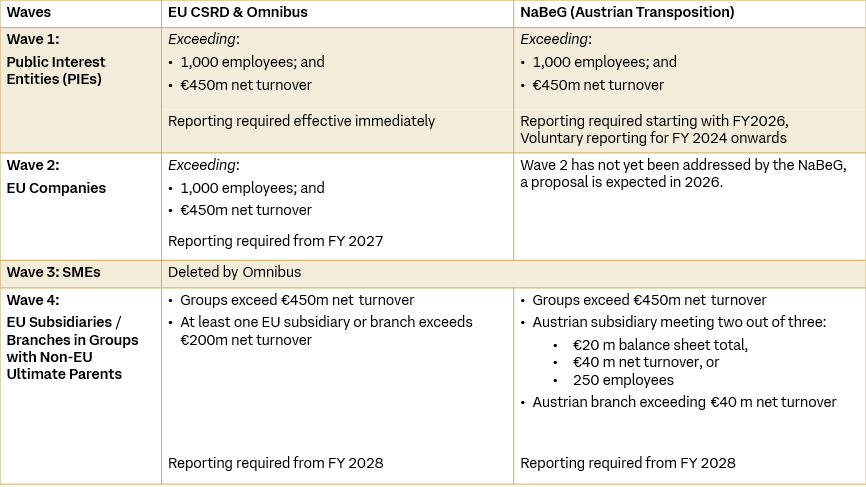

Most notably, Omnibus I raises the CSRD applicability thresholds, reducing the number of companies in scope. From FY 2027 (Wave 2), only EU companies with over 1,000 employees and a net turnover exceeding €450 million must report, exempting many smaller entities. Small and medium-sized entities (formerly Wave 3) have been fully exempted from reporting requirements. EU subsidiaries of non-EU headquartered groups (Wave 4) are subject to the reporting requirements if the non-EU group generates over €450 million in EU net turnover across the last two financial years and the EU subsidiary or branch itself has a net turnover of €200 million in the previous financial year. Member States may grant transitional relief for FY 2025 and 2026 to companies that no longer meet the new, higher thresholds. Omnibus I also limits mandatory sustainability data requests from non-CSRD business partners, introduces exemptions for financial holding companies, and allows protection of sensitive information.

Austria’s transposition – The Sustainability Reporting Act

A phased approach

The NaBeG first entered parliamentary review in January 2025 and therefore after the July 2024 deadline for transposition of the CSRD had passed. The process was put on hold following the publication of Omnibus I by the European Commission. The NaBeG re-entered parliamentary review in late 2025. It was passed by the Parliament in January 2026 and entered into force on 19 February 2026. It transposes CSRD requirements in stages, keeping with the EU’s ‘waves’ structure.

The law will apply immediately to undertakings with existing reporting requirements, specifically large public-interest entities (PIEs) that must produce CSRD-compliant sustainability reports for financial years beginning on or after 1 January 2024. Transitional provisions state that obligations do not apply for financial years ending before NaBeG enters into force, although companies may still voluntarily adopt Wave 1 obligations for financial years starting on 1 January 2024. In line with Omnibus I amendments, companies previously in scope but now falling below the new thresholds (€450 million in net turnover and 1,000 employees on an annual average), are exempt from these new obligations. However, these companies may voluntarily opt into the CSRD/ESRS regime.

Wave 2, covering large undertakings not previously subject to similar reporting requirements, are not yet addressed by the NaBeG. The Austrian legislator has explicitly indicated that a new legislative package to cover this group is expected in the first half of 2026. Full compliance with the CSRD for these entities will therefore follow at a later stage. The upcoming legislation is expected to reflect the latest amendments introduced by Omnibus I.

The newly introduced Drittlandunternehmen-Berichterstattungsgesetz (DriBeG) addresses CSRD’s Wave 4, imposing sustainability reporting requirements on Austrian subsidiaries and branches of non-EU groups with significant EU presence for financial years starting 2028. At the group level, if a non-EU parent generates more than €450 million turnover within the EU across the last two years, DriBeG obligations are triggered. Notably, the DriBeG only requires the Austrian subsidiary to meet ‘large company’ thresholds under Section 221(3) UGB (meeting two out of three – €20 million balance sheet total, €40 million net turnover, or 250 employees), which is considerably lower than the updated EU threshold of €200 million turnover for EU subsidiaries or branches of non-EU undertakings. This discrepancy between national and EU law appears to be the result of overlapping legislative procedures and is likely to be harmonised through future amendments.

Reporting content, format, and enforcement

The NaBeG mandates full alignment with the ESRS, emphasizing the double materiality principle. Companies must include detailed value chain disclosures. NaBeG reporting must cover the company’s business model, sustainability strategy, and internal governance framework. For the first three years, companies may document their efforts to obtain value chain information if it is unavailable. Reports must be submitted in a single electronic format, with digital tagging for all sustainability information, including disclosure required under the Taxonomy Regulation.

Administrative fines may be imposed for non-reporting, late filing, or inaccurate reporting. Furthermore coercive penalties may be imposed on legal representatives. Higher penalties may be imposed in cases involving large entities or entities of public interest, or in cases of repeated non-compliance. Sanctions for content-related errors only apply if a correction request is ignored, allowing for an initial adaptation period in the first three years. Both individual and consolidated sustainability reports require mandatory independent external assurance, which may be provided by the company’s statutory auditor or an accredited independent assurance services provider meeting NaBeG's independence, qualifications, and supervision requirements. The EU-wide limited assurance standard has been postponed by Omnibus I until July 2027, requiring the use of national standards in the meantime.

What businesses should look out for

The NaBeG aims for efficient transposition of the evolving and streamlined EU framework for corporate sustainability reporting. While the increased thresholds under Omnibus I reduce the regulatory burden for many companies, large public-interest entities and non-EU groups with a significant EU presence remain subject to comprehensive compliance requirements. Businesses should anticipate further legislative developments, particularly affecting Wave 2 companies, and expect a likely harmonization of national thresholds for non-EU subsidiaries and branches with EU requirements. The European Commission is currently updating the ESRS as part of Omnibus I, underscoring the dynamic nature of the reporting landscape. Proactive engagement with these developments and continuous monitoring of relevant regulation will be crucial for effective sustainability reporting.

As Austria’s NaBeG illustrates, the Omnibus I simplifications are fundamentally reshaping national sustainability frameworks. It is essential to understand how each Member State transposes these amendments – especially given that five jurisdictions have yet to transpose the original CSRD. For clarity on this evolving landscape, please see our interactive CSRD & Omnibus Implementation Tracker map which offers EU27 country snapshots of statuses, “gold-plating”, translation mandates and local currency thresholds. For deeper insights, you also have the option to subscribe to our monthly CSRD transposition updates and sign up to our detailed CSRD platform.

/Passle/581a17a93d947604e43db2f0/MediaLibrary/Images/2025-06-26-07-36-45-942-685cf88d527dd493930422da.jpg)

/Passle/581a17a93d947604e43db2f0/MediaLibrary/Images/2025-09-17-09-53-38-972-68ca85228206a7b6398617e6.jpg)

/Passle/581a17a93d947604e43db2f0/MediaLibrary/Images/2025-10-21-10-30-43-502-68f760d3a94b3b874acc7f85.png)